I Make Mortgages Make Sense

I am available seven days a week & 8am - 8pm to answer all your mortgage questions.

A Better Way to Your Next Home Loan

I Make Mortgages Make Sense

I am available seven days a week & 8am - 8pm to answer all your mortgage questions.

Mortgage FAQ

Niko Kramer | Mortgage Loan Officer | Satori Mortgage | NMLS #2180891Answers to common questions about working with Niko Kramer, the mortgage process, and the loan programs available to homebuyers, homeowners, and self-employed borrowers across 12 states.

About Niko Kramer

Who is Niko Kramer?

Niko Kramer is a licensed Mortgage Loan Officer with Satori Mortgage, NMLS #2180891. He helps homebuyers, homeowners, and self-employed borrowers across 12 states find the right home loan.

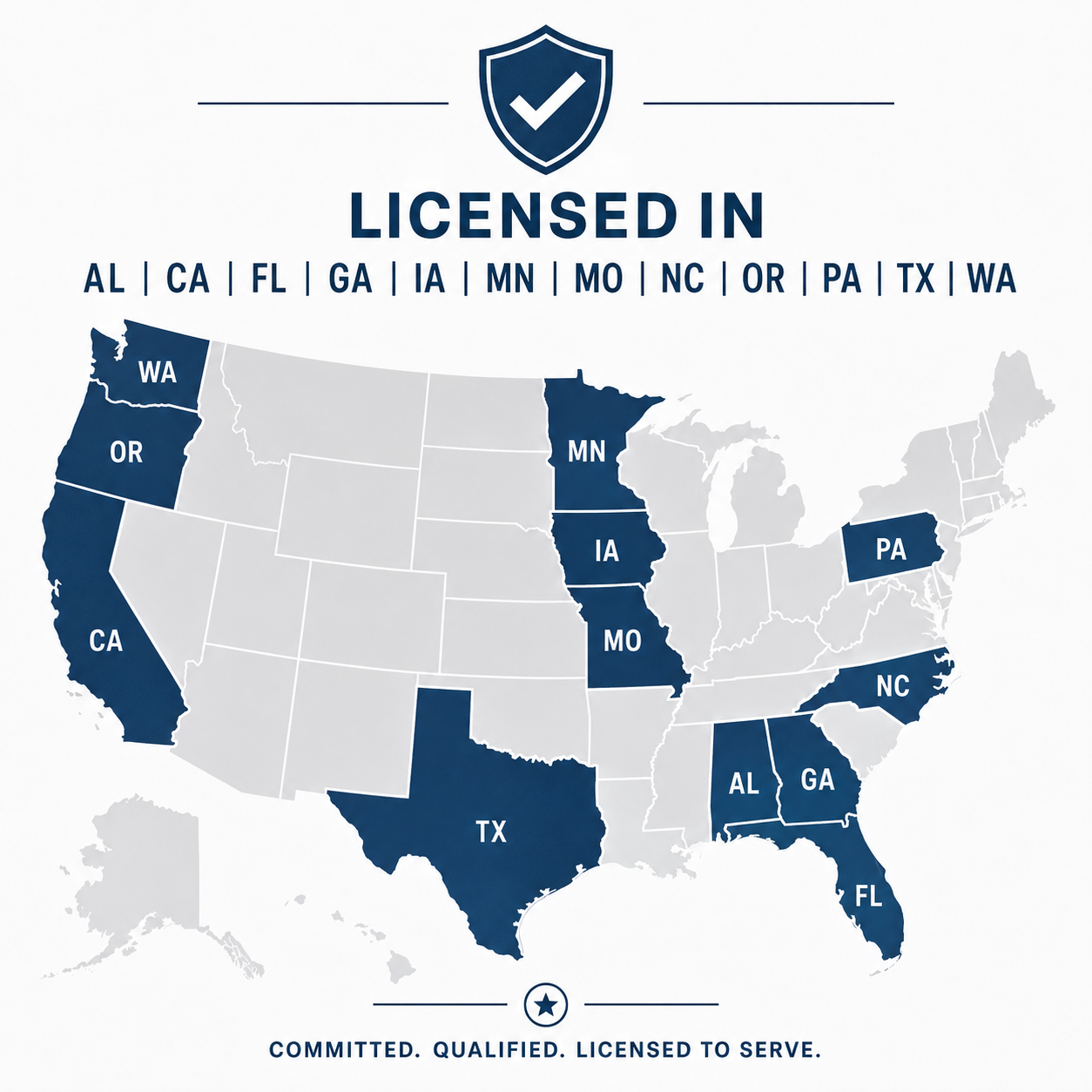

What states is Niko Kramer licensed in?

Niko Kramer is licensed to originate mortgages in Texas, Oregon, California, North Carolina, Florida, Minnesota, Washington, Alabama, Georgia, Iowa, Missouri, and Pennsylvania.

What types of home loans does Niko Kramer offer?

Niko offers Conventional, FHA, VA, USDA, Jumbo, and Bank Statement / Self-Employed loans, along with Refinance, VA IRRRL, and New Construction financing.

How do I contact Niko Kramer or start an application?

You can reach Niko at niko@satorimortgage.com or (512) 270-2835, or start your application using the buttons on this site. Learn more at nikokramer.com.

The Mortgage Process

What is the difference between pre-qualification and pre-approval?

A pre-qualification is an early estimate based on information you share, while a pre-approval involves a review of your documentation and credit. A pre-approval generally carries more weight with sellers. Niko can explain which step fits where you are.

What documents do I need to apply for a mortgage?

Most applications start with recent pay stubs, W-2s or tax returns, bank statements, and a photo ID. Self-employed borrowers may provide additional business documentation. Niko will give you a checklist tailored to your loan program.

How long does the mortgage process usually take?

Timelines vary by loan program, property, and how quickly documents are provided, but many purchase loans move from application to closing within a few weeks. Niko keeps you updated at each step.

What credit score do I need to buy a home?

Credit requirements depend on the loan program. Government-backed programs such as FHA and VA are often more flexible than conventional financing. Niko can review your credit and explain which programs may be available for your situation.

How much do I need for a down payment?

Down payment needs depend on the loan program and your situation. Some programs are designed for lower down payments for eligible borrowers, while others require more. Niko can walk you through the options for your scenario.

Loan Programs

What is the difference between FHA, VA, and conventional loans?

FHA loans are government-insured and often used by first-time buyers; VA loans are available to eligible veterans, service members, and surviving spouses; conventional loans are not government-backed and follow their own guidelines. Each has different eligibility and cost structures. Niko can compare them for your goals.

Can self-employed borrowers qualify for a mortgage?

Yes. Self-employed and 1099 borrowers who may not show traditional W-2 income can often be served through bank statement programs, which evaluate income differently than conventional documentation. Niko works regularly with self-employed borrowers to find the right fit.

What is a VA IRRRL?

A VA IRRRL (Interest Rate Reduction Refinance Loan) is a streamlined refinance option for eligible homeowners who already have a VA loan. It is designed to simplify refinancing an existing VA mortgage. Niko can confirm whether you are eligible.

Do I have to use the builder's preferred lender for a new construction home?

In most cases, no. You are generally not required to use a builder's preferred or in-house lender, even when incentives are offered for doing so, and you typically have the right to shop and compare financing. Niko can help you weigh the options.

Equal Housing Opportunity. All loans subject to credit and property approval; not all applicants will qualify. Information provided here is general and not a commitment to lend.

My Loan Process

Fast Track

JOIN OUR NEWSLETTER